Are you retiring or already in retirement?

Are you aware that you can leverage your Qualified Retirement Funds to avail yourself of the Long-Term Care coverage?

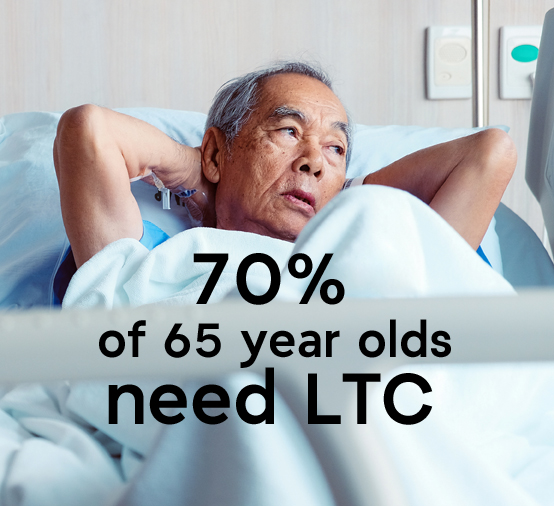

Statistics show that a person turning 65 today has almost 70% chance of needing some type of Long-Term Care, Home and Assisted Care services and support in their remaining years.

The good news is current solutions are available through Asset Based Long-Term Care coming from Qualified Funds, IRA’s, 401k’s, 403b’s and others. Non-Qualified funds can also be used to buy Long-Term Care.

Aside from these solutions, Traditional Long-Term Care is available as an option for your Long-Term Care needs.

It is important to know that Medicare does not provide or cover most Long-Term Care coverage unless medical care is needed. Long-Term Care is vital for making sure that adults can always live a rich and happy active life, no matter how their health needs may change in time.

Asset Based Long-Term Care Insurance Policies

There are several benefits to individuals who are planning for their Long-Term care needs. One of the primary benefits is to provide peace of mind.

Knowing that having the coverage in place can help you feel more secure about the future and the ability to pay for Long-Term Care services when that time comes.

- Asset Based Long-Term Care has been available in the marketplace for 35 years

- Offered by a mutual insurance company with an A+ superior from AM Best rating

- Retirement LTC is here to help secure peace of mind for you and your loved ones

Myths vs. Facts

Myth #1: “A government program will take care of me.”

- Government programs are tough to qualify for.

- Public programs like Medicare, Medicaid and veterans’ services may help pay for some LTC services in certain circumstances. Yet programs have very specific rules.

- When Medicaid does pay someone’s LTC costs, federal law requires states to recover money spent from the person’s estate.

- Government programs are limited by availability and financial resources.

Myth #2: “I can save the money I’ll need for LTC services.”

- Long-term care services can be very expensive.

- These costs are a huge financial risk to older adults’ retirement dollars.

- Those who plan to pay LTC expenses could quickly wipe out their lifetime savings. The avg. cost for a 1 year stay in a private nursing home is $83,580.

Myth #3: “Only old people need LTC services.”

- Among adults age 65 and older, about 70 percent need some help with the activities of daily living as they age.

- It’s wise to look into LTC protection before services are needed for two primary reasons: Cost and need.

Myth #4: “I don’t need separate LTC protection because I have health insurance.”

- LTC protection is not the same as health insurance.

- Health insurance helps pay for medical care only.

- LTC benefits help support costly LTC services.

- LTC services generally are required by those with chronic, progressive illnesses, accidents or advanced aging.

Myth #5: “LTC protection pays for nursing home care only.”

- LTC benefits help people access the care they want.

- LTC protection provides options in a range of medical, personal and social services in a variety of settings.

- LTC benefits can provide for caregiver training, care coordination, respite care and hospice care.

- Government programs are limited by availability and financial resources.

Retirement LTC

Call us at 619-372-6449

EMAIL: info@RetirementLTC.com

ADDRESS: 5703 Oberlin Dr., Suite 101, San Diego, CA 92121

OFFICE HOURS:

Monday through Friday: 7am to 6pm

Saturday: 9am to 3pm

Sunday: Closed